Income Tax Act 1961, Sections 207–219 · FY 2025-26 · By ASAS & Associates / KarSahi

Most salaried employees are familiar with TDS — the tax deducted from their salary every month by their employer. But for anyone with income beyond salary, or for business owners and professionals, there is another equally important obligation: advance tax. Ignoring it can result in significant interest charges that compound every month until you settle the dues.

What is Advance Tax?

Advance tax is essentially the system of paying your estimated income tax liability in instalments during the financial year itself, rather than in one lump sum at the end. The underlying principle is that the government wants to collect tax as and when income is earned — just as your employer deducts TDS from your salary each month. The obligation to pay advance tax arises when your total estimated tax liability for the year, after accounting for TDS that will be deducted, exceeds ₹10,000.

Who Must Pay Advance Tax?

Any individual, HUF, firm, or company whose estimated tax liability exceeds ₹10,000 after TDS credit must pay advance tax. For salaried employees whose employer deducts TDS fully, there is usually no separate advance tax obligation. However, if you have side income — rental income, interest from fixed deposits, capital gains, freelance income, or business income — the TDS on these sources may not be sufficient to cover your total liability, making you liable for advance tax on the balance.

Senior citizens aged 60 years and above who do not have income from business or profession are completely exempt from paying advance tax. They can pay all their taxes at the time of filing their return without attracting any interest.

Taxpayers who have opted for the presumptive taxation scheme under Section 44AD or 44ADA have a simplified obligation: they pay 100% of their advance tax in a single instalment due on 15th March.

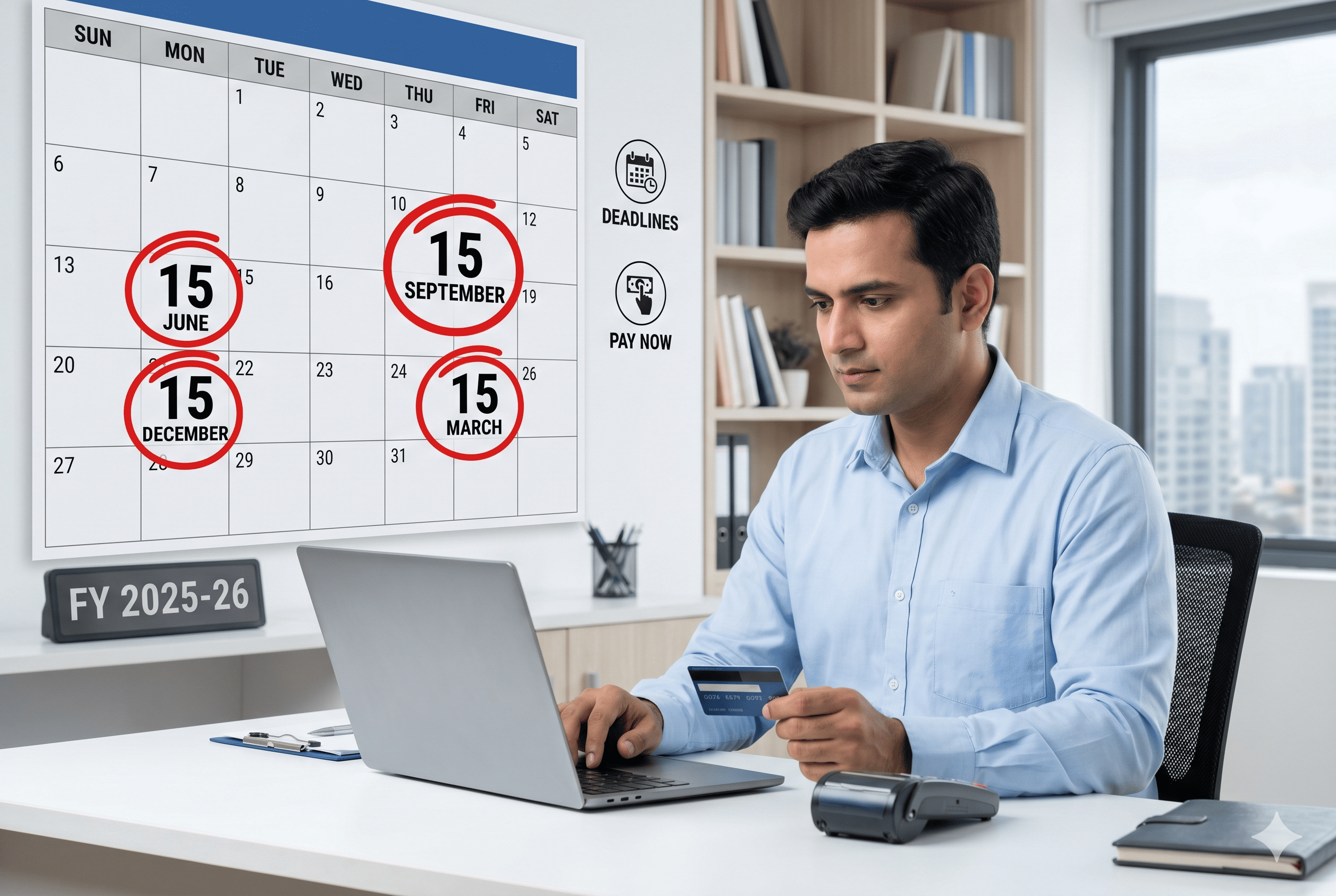

The Instalment Schedule for FY 2025-26

For all taxpayers other than presumptive scheme declarants, advance tax is payable in four instalments during the financial year. By 15th June, 15% of your estimated annual tax liability must be paid. By 15th September, this cumulative payment must reach 45%. By 15th December, it must reach 75%. The final instalment, bringing the cumulative payment to 100%, is due by 15th March 2026.

These percentages are applied to your estimated tax liability for the full year. If your income fluctuates — for example, because you receive a large capital gain in December — you should recalculate your liability and adjust the remaining instalments accordingly.

How to Calculate Your Advance Tax

Start by estimating your total income for the financial year across all sources: salary, business or professional income, rental income, interest income, and any anticipated capital gains. From this, subtract eligible deductions under Chapter VI-A (such as 80C, 80D, and 80E) to arrive at your estimated taxable income. Apply the applicable tax slab rates and add surcharge and health and education cess at 4% to get your gross tax liability. Finally, deduct the TDS that is expected to be deducted from your income during the year. If the balance exceeds ₹10,000, you are required to pay advance tax.

Payment is made online through the Income Tax portal at tax.gov.in by selecting ‘e-Pay Tax’, choosing Challan 280, and selecting the option ‘(100) Advance Tax’. Keep the challan receipt for your records — you will need it while filing your ITR.

Interest Penalties for Default

Three sections of the Income Tax Act deal with interest for failure to pay advance tax. Section 234B applies when you have paid less than 90% of your assessed tax liability by 31st March. Interest is charged at 1% per month from 1st April until the date of assessment. Section 234C applies when each instalment is short of the prescribed percentage. Interest is charged at 1% per month for three months per instalment (except the last instalment, where it is charged for one month). Section 234A applies when your return is filed after the due date with unpaid tax — again at 1% per month from the due date to the actual filing date.

These interest charges are not penalties in the strict sense — you do not get to appeal against them. They are mandatory and calculated automatically by the system. The only way to avoid them is to pay your advance tax on time.

Common Mistakes to Avoid

Many taxpayers underestimate their capital gains from stock market transactions or mutual fund redemptions during the year, leading to a shortfall in advance tax. Similarly, freelancers and consultants who receive large payments in the latter half of the year often discover too late that they owe advance tax interest for the earlier quarters. The safest approach is to review your income at least once per quarter and recalibrate your advance tax payment accordingly.

KarSahi calculates your advance tax liability across all four quarters as part of the Personal Income Tax Plan (₹9,999/year). Never pay unnecessary interest on missed instalments. Book at karsahi.com.

1 Comment

A WordPress Commenter

March 16, 2026Hi, this is a comment.

To get started with moderating, editing, and deleting comments, please visit the Comments screen in the dashboard.

Commenter avatars come from Gravatar.