Income Tax Act 1961, Sections 44AD / 44ADA / 44AE · FY 2025-26 · By ASAS & Associates / KarSahi

If you run a business, practice a profession, or earn income from self-employment, you face a choice that most employees never think about: how to account for your income and expenses for tax purposes. The Income Tax Act offers a simplified path called the presumptive taxation scheme for eligible taxpayers, and a more rigorous but flexible path of maintaining regular books of accounts. Choosing the wrong path — or switching carelessly — can have consequences that last five years.

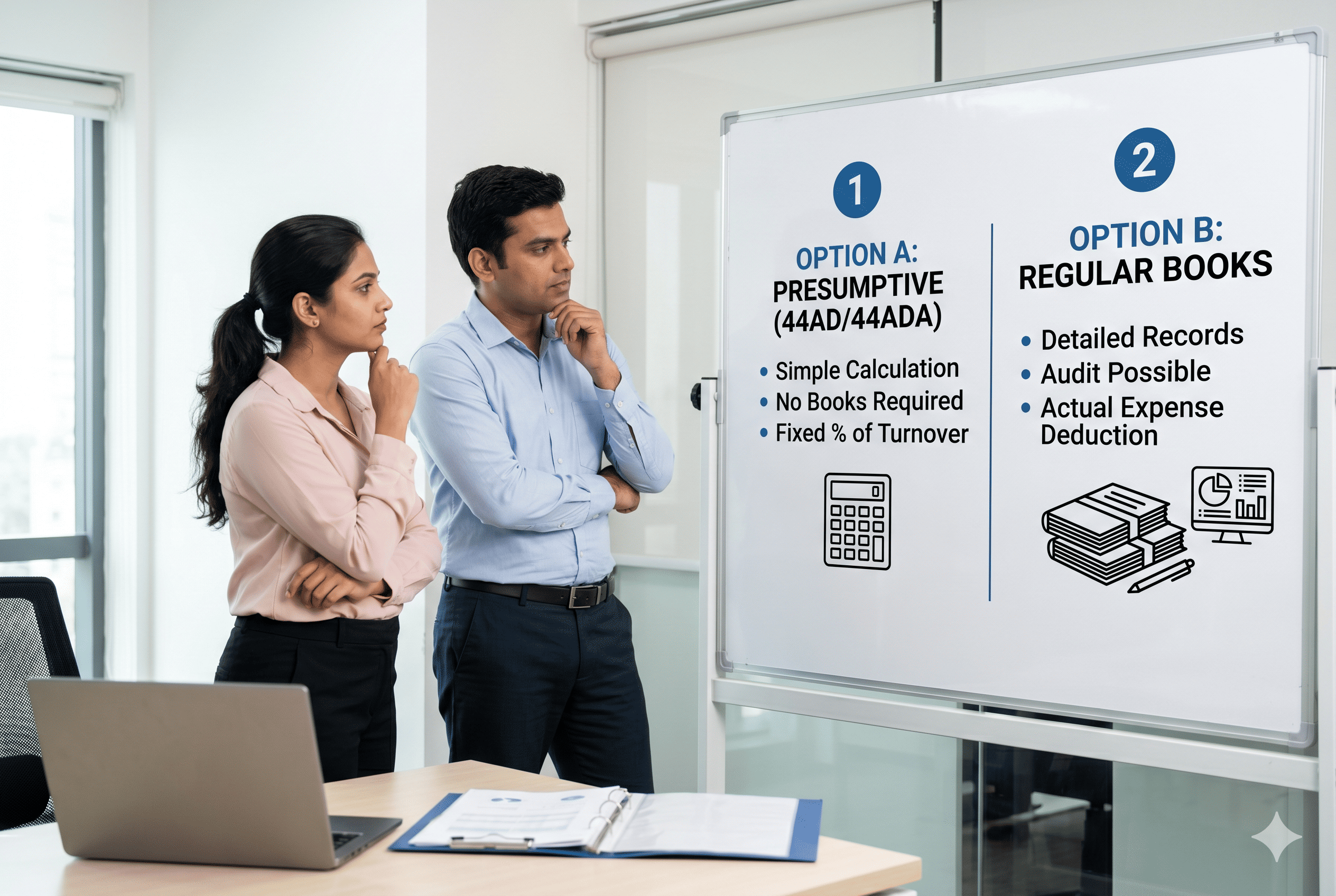

The Presumptive Taxation Concept

Under the presumptive taxation scheme, the Income Tax Department acknowledges that small businesses and professionals cannot always maintain detailed books of accounts. To simplify compliance, it allows eligible taxpayers to declare a fixed percentage of their gross receipts or turnover as their income — without needing to prove their actual expenses. This deemed income is then taxed at normal slab rates.

The trade-off is straightforward. You give up the ability to claim actual business expenses and deductions, but in return you are freed from maintaining complex financial records, preparing a balance sheet and P&L account, and in most cases, from the obligation of a tax audit.

Section 44AD — Presumptive Tax for Businesses

Section 44AD applies to resident individuals, Hindu Undivided Families, and firms other than LLPs who are carrying on any eligible business. The eligible businesses are broadly defined but exclude certain specific categories: commission agents and brokers, persons earning income by way of brokerage, professionals covered under Section 44ADA, and persons covered under Section 44AE (goods carriage owners).

Under 44AD, your business income is deemed to be 6% of your total turnover if the receipts are through banking channels or digital payments. If any part of the turnover is received in cash, that portion is deemed to yield 8% income. You can declare a higher profit voluntarily if your actual profit exceeds these percentages.

The turnover threshold for Section 44AD was enhanced to ₹3 crore, provided that cash receipts during the year do not exceed 5% of total receipts (and cash payments do not exceed 5% of total payments). If your cash transactions exceed this threshold, the older limit of ₹2 crore applies.

One critical rule governs the decision to opt for 44AD: if you choose 44AD in a financial year and later decide to opt out — either because your actual profits are much higher, or because you want to carry forward losses — you cannot re-enter the scheme for the next five financial years. During those five years, you must maintain regular books of accounts and are subject to audit under Section 44AB if your income from business exceeds the basic exemption limit. This five-year lock-out rule means the decision to adopt 44AD must be considered carefully.

Section 44ADA — Presumptive Tax for Specified Professionals

Section 44ADA was introduced specifically for professionals who found the presumptive scheme under 44AD inapplicable to them. It covers resident individual professionals engaged in specified occupations: legal practitioners (advocates and solicitors), medical practitioners, engineers, architects, chartered accountants, cost accountants, company secretaries, technical consultants, interior designers, and film artists.

Under 44ADA, your professional income is deemed to be 50% of your gross receipts. If your actual net profit from practice exceeds 50% of gross receipts, you can voluntarily declare the higher figure. If your actual profit is less than 50%, you cannot declare a lower figure without inviting the obligation of a tax audit.

The threshold for 44ADA was revised to ₹75 lakh, with the same digital transaction condition as 44AD applying for the higher threshold. The scheme requires that advance tax be paid in a single instalment by 15th March, simplifying the quarterly obligation.

Unlike 44AD, there is no five-year lock-out rule for 44ADA — you can switch between 44ADA and the regular scheme from year to year, though doing so requires you to maintain proper books of accounts in the years you opt out.

Section 44AE — Presumptive Tax for Goods Carriage Owners

Section 44AE applies to businesses involving the plying, hiring, or leasing of goods carriages. Taxpayers owning up to 10 goods carriages at any time during the year can declare income on a per-vehicle, per-month basis as specified in the section, without maintaining detailed books. This provision is specific to the transport sector and does not interact with the broader 44AD scheme.

The Regular Scheme — When Presumptive Does Not Apply

If your turnover or gross receipts exceed the prescribed thresholds, or if you are an LLP, or if you deal in commission or brokerage income, you must use the regular scheme. This means maintaining proper books of accounts including a cash book, journal, ledger, and vouchers. At the year end, you prepare a profit and loss account and balance sheet. Your actual income after deducting all legitimate business expenses is your taxable profit.

The regular scheme offers far greater flexibility. You can claim depreciation on business assets, deduct rent, salaries, interest on business loans, professional fees, and all other genuine business expenses. If your actual profit margin is thin — perhaps 2% to 3% of turnover — the regular scheme will result in far less tax than the presumptive scheme’s deemed 6% or 8%.

The downside is compliance burden. You need an accountant, proper invoicing discipline, and a bank account that accurately reflects business transactions. If your turnover crosses ₹1 crore (or ₹10 crore with 95% digital transactions), a tax audit by a chartered accountant under Section 44AB becomes mandatory.

When Does a Tax Audit Become Mandatory?

A tax audit is required when a business’s turnover exceeds ₹1 crore (or ₹10 crore in the digital transaction exception scenario). For professionals, the threshold is ₹50 lakh of gross receipts. Additionally, if you have opted for the presumptive scheme and declare profit below the deemed percentage — for example, you have opted for 44AD but your actual profit is only 4% — an audit is mandatory if your income exceeds the basic exemption limit. The audit must be completed by a chartered accountant and the report submitted (Form 3CA/3CB and 3CD) along with your ITR before the due date.

Making the Right Choice

The right scheme depends on your actual profit margin relative to the deemed rate. If your business genuinely earns 10% or 15% profit on turnover, adopting 44AD means you pay tax on only 6% — a significant saving. If your actual profit margin is only 4% or 5%, paying tax on the deemed 6% may be marginally higher than your actual liability under the regular scheme. For professionals, the 50% deemed rate under 44ADA is generous if your actual expenses are less than 50% of receipts.

However, tax savings is not the only consideration. If you have business losses to carry forward, the regular scheme is the only option — you cannot declare a loss under the presumptive scheme. If you plan to apply for a bank loan or visa where financial statements are required, maintaining regular books serves you better. And if your business is growing and turnover is likely to cross the threshold in the next one or two years, entering the regular scheme early avoids the complexity of a mid-course change.

Not sure which scheme to opt for? KarSahi’s CA will review your receipts, expenses, and future plans to recommend the most tax-efficient approach — all in a 30-minute live session. Book at karsahi.com.