Finance Act 2025 · Updated slabs for AY 2026-27 · By ASAS & Associates / KarSahi

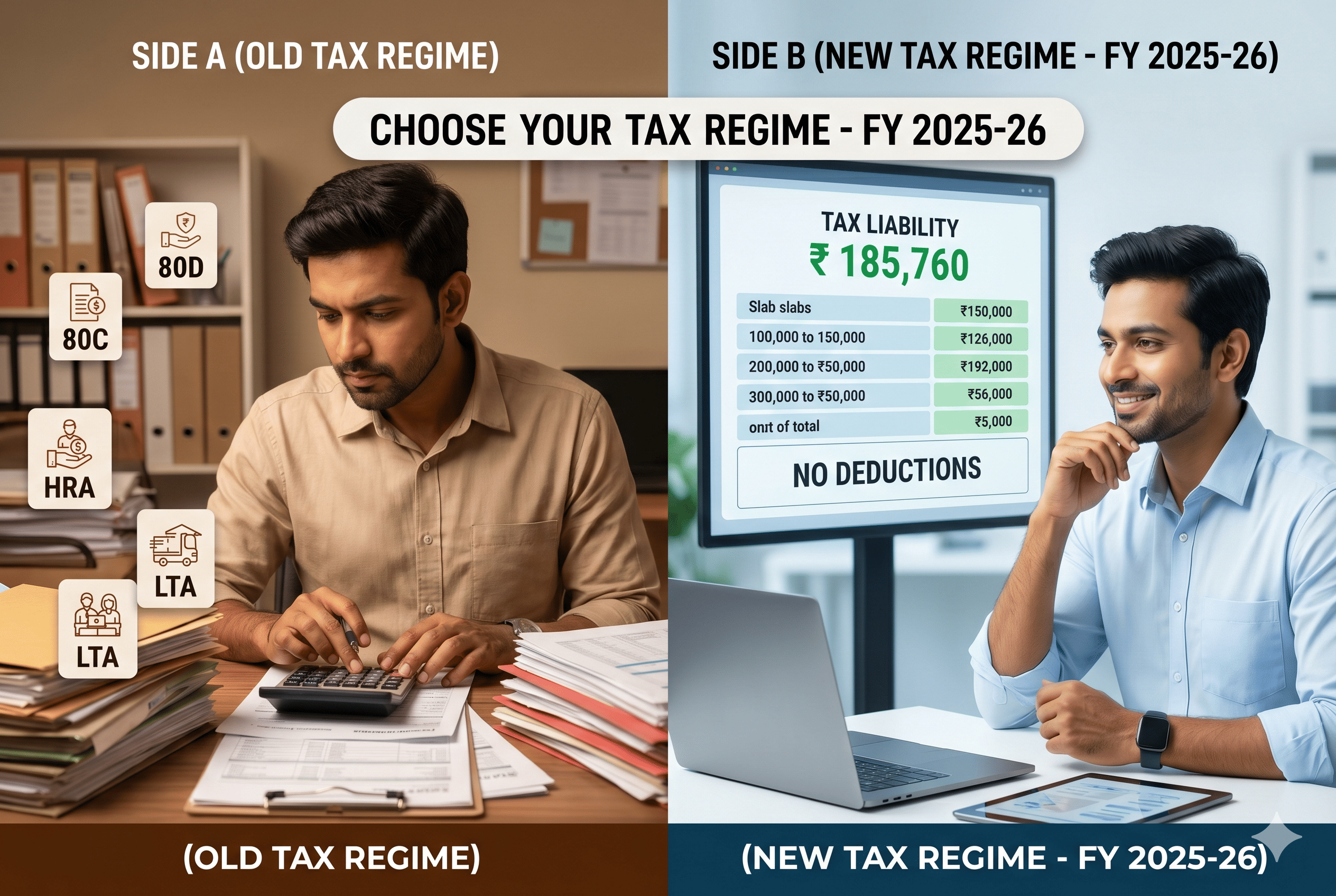

One of the most debated questions among Indian taxpayers every year is whether to opt for the Old Tax Regime or the New Tax Regime. The Finance Act 2020 introduced the New Regime as an optional, simplified alternative with lower tax rates but no deductions. The Finance Act 2023 made the New Regime the default, meaning if you do not actively choose the Old Regime, you are automatically taxed under the New one. The Finance Act 2025 further revised the New Regime slabs, making it even more attractive for a large segment of taxpayers. This guide will help you determine which regime actually saves you more money.

The New Tax Regime — Default from FY 2025-26

The New Regime for FY 2025-26 features revised slabs: income up to ₹4 lakh is nil; income between ₹4 lakh and ₹8 lakh is taxed at 5%; between ₹8 lakh and ₹12 lakh at 10%; between ₹12 lakh and ₹16 lakh at 15%; between ₹16 lakh and ₹20 lakh at 20%; between ₹20 lakh and ₹24 lakh at 25%; and above ₹24 lakh at 30%.

Crucially, a rebate under Section 87A ensures that individuals with income up to ₹12 lakh pay zero income tax under the New Regime — the tax is fully rebated. For salaried individuals, the standard deduction of ₹75,000 applies under the New Regime, effectively making income up to ₹12.75 lakh tax-free.

The New Regime does not allow most of the traditional deductions and exemptions — no 80C, no 80D, no HRA exemption, no LTA exemption, and no interest deduction on home loans for self-occupied property. The NPS employer contribution under Section 80CCD(2) is, however, available even under the New Regime, which is a notable exception.

The Old Tax Regime — For Those With Significant Deductions

The Old Regime retains the traditional slab structure: nil tax up to ₹2.5 lakh for individuals below 60 years; 5% from ₹2.5 lakh to ₹5 lakh; 20% from ₹5 lakh to ₹10 lakh; and 30% above ₹10 lakh. Senior citizens (60 to 80 years) have a basic exemption of ₹3 lakh, while super senior citizens above 80 years have an exemption of ₹5 lakh.

The Old Regime’s advantage lies entirely in the deductions it permits. Section 80C allows a deduction of up to ₹1.5 lakh for investments in life insurance, PPF, ELSS mutual funds, employee provident fund contributions, National Savings Certificates, school tuition fees, and home loan principal repayment. Section 80D allows deduction of health insurance premiums — up to ₹25,000 for self and family, and up to ₹50,000 for senior citizen parents. Interest on a housing loan for a self-occupied property is deductible up to ₹2 lakh under Section 24(b). The HRA exemption under Section 10(13A) can be substantial for salaried employees in metro cities. The standard deduction under the Old Regime is ₹50,000 for salaried individuals.

How to Choose — The Decision Framework

The choice between regimes comes down to one comparison: is your total eligible deduction amount large enough that the Old Regime’s after-deduction tax is lower than the New Regime’s tax on your gross income?

For taxpayers with income up to ₹12 lakh (₹12.75 lakh for salaried), the New Regime is almost always better due to the zero-tax benefit under the rebate. There is no combination of Old Regime deductions that can match this.

For taxpayers with higher income, the calculation becomes more nuanced. Consider someone earning ₹15 lakh annually. Under the New Regime, the tax on ₹15 lakh (after ₹75,000 standard deduction, net ₹14.25 lakh taxable income) works out to approximately ₹1.70 lakh. Under the Old Regime, if the same person claims ₹1.5 lakh under 80C, ₹25,000 under 80D, ₹2 lakh as home loan interest deduction, and ₹50,000 standard deduction — total deductions of ₹4.25 lakh — the taxable income is ₹10.75 lakh, and the tax works out to approximately ₹1.37 lakh. In this case, the Old Regime saves about ₹33,000. But if this person has no home loan and minimal investments, the New Regime wins.

The approximate break-even is often cited at total deductions of around ₹3.75 lakh for taxpayers in the 30% bracket. If your total deductions — 80C plus 80D plus home loan interest plus any other allowable deductions — comfortably exceed this figure, the Old Regime is likely better. If not, the New Regime is simpler and often cheaper.

Specific Situations Where the Old Regime Helps

Taxpayers who have home loans in metro cities benefit significantly from the combination of principal repayment under 80C and interest deduction under Section 24(b). Parents paying for higher education benefit from Section 80E, which allows full deduction of education loan interest for up to eight years. Individuals with old life insurance policies and long-standing PPF accounts may find the 80C limit exhausted before they need to make any fresh investment. For all these categories, the Old Regime typically delivers meaningful savings.

Specific Situations Where the New Regime Helps

Young professionals who have not started investing, or who invest primarily in equity markets without insurance products, often find that their actual 80C investments are low. For them, the New Regime’s lower rates with no investment obligation is simply more efficient. NRIs are another category who benefit from the New Regime: most deductions available under the Old Regime (HRA, LTA, 80C for certain instruments) are either unavailable or less relevant for NRIs, making the New Regime’s lower rates more attractive.

Switching Between Regimes

Salaried employees have the flexibility to switch between the two regimes every year. You inform your employer of your choice at the start of the year, and the employer deducts TDS accordingly. You can also change your choice when filing your ITR.

For business income taxpayers — sole proprietors, freelancers, and professionals — the rules are stricter. You can switch from the New Regime to the Old Regime, but once you switch back to the New Regime from the Old Regime, you can never return to the Old Regime. This effectively means business income taxpayers have a one-time option to switch back to the New Regime, after which the New Regime becomes permanent. The choice should therefore be made after careful analysis, not year by year.

If you fail to file your return by the due date, the New Regime is applied by default for that year and you lose the option to choose the Old Regime for that assessment year.

KarSahi’s CA compares both regimes for your specific income, investments, and deductions during the live Google Meet session and recommends the one that saves you the most tax. Book at karsahi.com.